Do We Work with Stripe, Adyen, PayFac, or Worldpay?

Wondering whether your business should use Stripe, Adyen, Worldpay, or a PayFac? Learn how modern payment infrastructure works and how to choose the best processor.

3/10/20264 min read

Businesses looking for a payment processor often ask the same question:

“Do you support Stripe, Adyen, Worldpay, or PayFac solutions?”

It’s a reasonable question. Platforms like Stripe, Adyen, and Worldpay are among the largest payment infrastructure providers in the world.

But choosing a payment processor is not just about selecting a brand name.

Modern businesses need a payment infrastructure strategy that supports growth, risk management, international payments, and scalability.

In this guide, we’ll cover:

What Stripe, Adyen, and Worldpay actually do

What a PayFac (Payment Facilitator) is

Why many companies use multiple payment processors

How businesses choose the best payment infrastructure in 2026

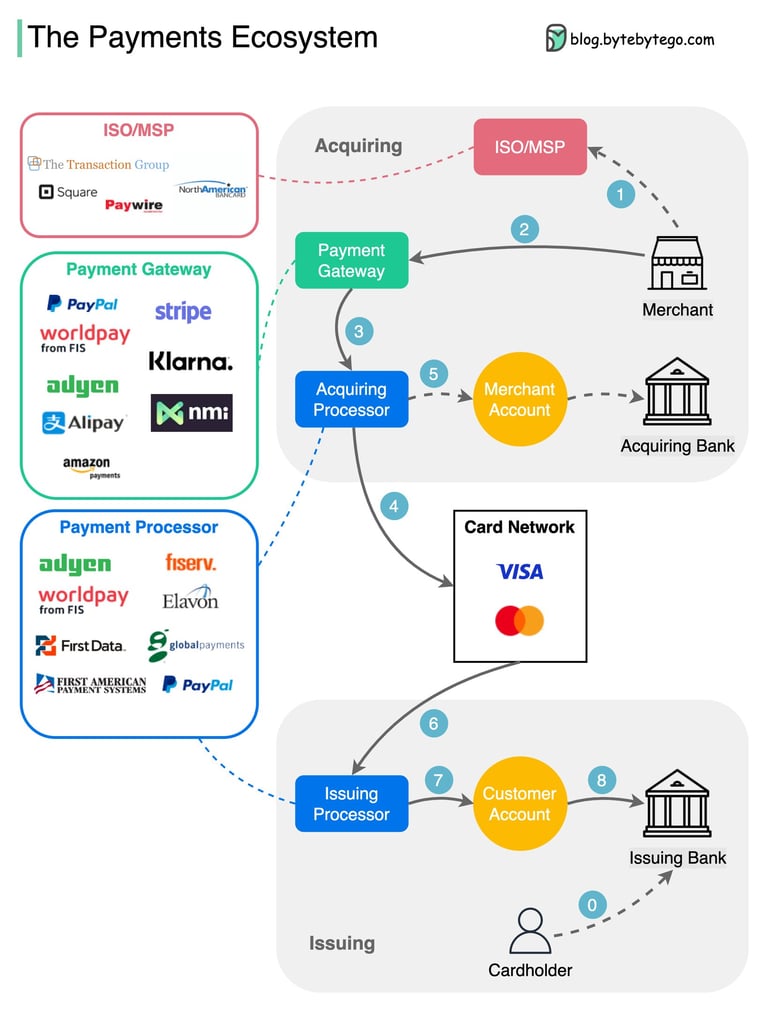

What Is a Payment Processor?

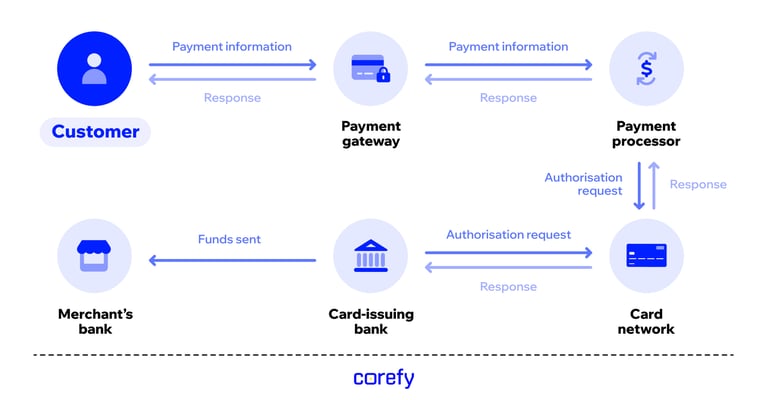

A payment processor is the technology that enables businesses to accept credit cards, debit cards, and digital payments.

When a customer makes a purchase online or in person, the processor connects several parties:

the customer’s bank

the merchant’s bank

the card network (Visa, Mastercard, etc.)

the payment gateway

This process happens in seconds, allowing funds to move securely between accounts.

Stripe vs Adyen vs Worldpay: What’s the Difference?

Many businesses researching payment processors compare platforms like Stripe, Adyen, and Worldpay.

While they all process payments, their ideal use cases are different.

Stripe

Stripe is widely known for:

developer-friendly APIs

easy ecommerce integration

strong SaaS billing tools

startup-friendly onboarding

Many SaaS and technology companies start with Stripe because it is easy to integrate into software platforms. Learn more about how payment processing works from Stripe’s payment guide.

Adyen

Adyen is typically used by:

global ecommerce brands

enterprise merchants

international marketplaces

It provides infrastructure for companies operating across multiple regions and currencies. Adyen global payments resource.

Worldpay

Worldpay is one of the largest merchant acquirers globally.

It is often used by:

large retailers

enterprise ecommerce platforms

high-volume merchants

It offers extensive acquiring bank relationships and global payment capabilities. Learn about Worldpay

What Is a PayFac (Payment Facilitator)?

A Payment Facilitator (PayFac) allows businesses to accept payments without opening a traditional merchant account directly with a bank.

Instead:

the PayFac operates the master merchant account

businesses become sub-merchants

This model enables:

faster onboarding

easier integrations

embedded payments for SaaS platforms

simplified compliance management

Many modern payment platforms operate using a variation of the PayFac model.

Why Many Businesses Use Multiple Payment Processors

One of the biggest misconceptions in payments is that a business should only use one payment processor.

In reality, many companies operate with multiple payment providers.

Reasons include:

Higher Approval Rates

Different processors connect to different acquiring banks.

Using multiple providers can improve transaction approval rates.

Risk Management

Some industries are considered higher risk.

Having access to multiple processors prevents sudden disruptions if one provider changes underwriting policies.

Global Payments Optimization

Payment preferences vary worldwide.

For example:

Europe prefers local payment methods

Asia uses alternative wallets

North America relies heavily on cards

Using multiple processors can improve international checkout performance.

How to Choose the Best Payment Processor for Your Business

Choosing the right payment infrastructure depends on several factors.

Business Model

SaaS, ecommerce, marketplaces, and subscription businesses often require different payment solutions.

Industry Risk Level

Some industries require specialized acquiring banks due to regulatory or fraud considerations.

Geographic Expansion

Businesses operating internationally need processors that support:

multiple currencies

local payment methods

regional acquiring banks

Scalability

The right payment processor should support your growth as transaction volume increases.

If you’re evaluating different processors, you may also find our guide helpful:

How to Choose the Right Payment Processor for Your Business (Step-by-Step Guide for 2026)

Why Businesses Work With Payment Infrastructure Advisors

Many companies assume they must choose a single processor and commit long-term.

However, payment consultants often take a processor-agnostic approach, meaning they evaluate multiple providers to determine the best solution.

This approach allows businesses to access:

enterprise payment platforms

PayFac infrastructure

specialized acquiring banks

scalable ecommerce payment stacks

Final Thoughts

Platforms like Stripe, Adyen, and Worldpay are powerful tools in the payments ecosystem.

However, the best payment solution depends on more than just choosing a processor.

The most successful businesses focus on building a flexible payment infrastructure that supports:

scalability

global payments

industry compliance

long-term growth

Understanding the available options is the first step toward choosing the right payment strategy.

How Harbor Payment Solutions Provides Access to Stripe, Adyen, PayFac, and Enterprise Payment Infrastructure

Many businesses assume they must choose one payment processor and commit to it long-term.

In reality, modern payment infrastructure works very differently.

At Harbor Payment Solutions, the goal is not to push a single platform. Instead, the focus is helping businesses identify and access the right payment infrastructure for their specific needs.

Because Harbor works across a network of payment providers, businesses can gain access to solutions including:

Stripe integrations for SaaS and software platforms

Adyen for global enterprise payment processing

Worldpay acquiring infrastructure for high-volume merchants

PayFac (Payment Facilitator) solutions for marketplaces and embedded payments

Specialized acquiring banks for regulated or higher-risk industries

This processor-agnostic approach allows Harbor to design payment solutions that are tailored to each business instead of forcing companies into a single platform.

Access to Multiple Payment Processors

Different payment processors are optimized for different business models.

For example:

SaaS platforms may benefit from Stripe’s developer-first infrastructure

Global ecommerce brands may prefer enterprise platforms like Adyen

Large retailers may require high-volume acquiring relationships

Because Harbor works with multiple payment ecosystems, businesses can choose the infrastructure that best supports their:

transaction volume

industry risk profile

geographic reach

long-term growth plans

Flexible Payment Infrastructure for Growing Businesses

One of the biggest challenges companies face is outgrowing their payment processor.

For example, businesses may encounter:

account restrictions

transaction limits

higher fees as volume grows

international payment limitations

By working with Harbor Payment Solutions, businesses can build a scalable payment stack that evolves as the company grows.

This may include:

multiple payment processors

alternative acquiring banks

optimized payment routing

specialized fraud and risk management tools

A Strategic Approach to Payment Processing

Rather than starting with a processor, Harbor begins with the business model.

Key factors evaluated include:

ecommerce vs SaaS vs marketplace models

domestic vs global transactions

regulatory requirements

expected growth in transaction volume

This allows businesses to implement payment infrastructure that supports both current operations and future expansion.

Ready to Improve Your Payment Processing?

Start with a free consultation and see how Harbor Payment Solutions can help your business save money and scale with confidence

© 2025. All rights reserved.

Professional, transparent payment processing services for businesses across the United States. Processing services provided through trusted processing partners. Harbor Payment Solutions operates as a consulting and advisory firm.

Powered by FX Web Ventures