Payment Processing Explained: A Complete Guide for Business Owners

Learn how payment processing works, what fees you are really paying, and how to avoid overpaying. A complete guide for small business owners.

12/18/20254 min read

What Is Payment Processing?

Payment processing is the system that allows your business to accept credit cards, debit cards, and digital payments from customers and deposit those funds into your bank account.

Behind every card transaction is a multi-step process involving banks, card networks, and payment technology providers. While it happens in seconds, each step carries a cost that ultimately appears on your monthly statement. Understanding how payment processing works for businesses helps clarify why fees exist and where your money actually goes.

At a high level, payment processing includes:

Authorization of the transaction

Secure transfer of funds

Settlement and deposit

Fraud and compliance protection

Reporting and reconciliation

Payment processing is one of the most critical systems behind every modern business, yet it is also one of the most misunderstood. Many business owners sign up for payment processing solutions, glance at their monthly statement, and move on without fully understanding how fees work or whether they are being overcharged.

This guide breaks down how payment processing works, what you are actually paying for, and how to avoid hidden costs, so you can make confident decisions for your business. Whether you run a retail store, restaurant, medical office, or service business, understanding this system directly impacts your bottom line.

How a Credit Card Transaction Works

Every card transaction follows the same basic path:

The customer presents their card or digital wallet

Your POS system sends the transaction for approval

The card network routes the request

The issuing bank approves or declines

Funds are settled and deposited into your account

This process involves major card networks like Visa, Mastercard, American Express, and Discover, as well as your processor and acquiring bank.

Each step introduces small costs that eventually appear on your statement. For a deeper breakdown of this flow and related fees, reviewing in-depth payment processing guides can help business owners better understand where those costs come from.

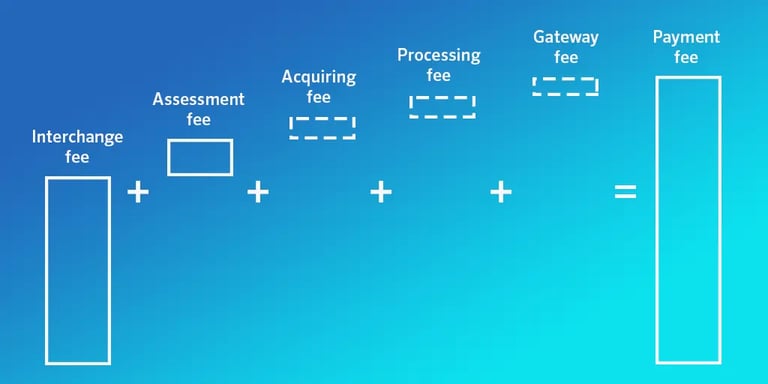

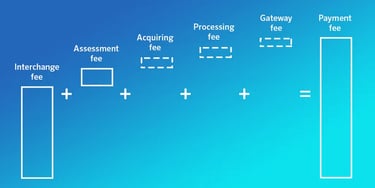

Understanding Payment Processing Fees

This is where most confusion and frustration occurs.

Your processing costs are typically made up of three main components:

1. Interchange Fees

Interchange fees are set by the card networks and paid to the issuing bank. These fees vary based on:

Card type (debit, credit, rewards)

How the card is accepted (tap, chip, online)

Industry type

Interchange fees are non-negotiable, but how they are passed to you matters.

2. Card Network Fees

These are assessment fees charged by card brands like Visa and Mastercard. They are smaller but unavoidable.

3. Processor Markup

This is where pricing varies the most. The processor markup is what your payment provider charges for:

Technology

Support

Risk management

Profit

This portion is negotiable, but many businesses never realize it.

Common Pricing Models Explained

Interchange Plus Pricing

This is the most transparent pricing model. You pay the true interchange cost plus a fixed markup.

Best for businesses that want visibility and long-term savings.

Flat Rate Pricing

A single percentage for all transactions. Simple, but often more expensive as volume grows.

Tiered Pricing

Transactions are grouped into qualified, mid-qualified, and non-qualified tiers. This model lacks transparency and is often where overcharging happens.

At Harbor Payment Solutions, our focus is helping merchants understand which model fits their transaction mix, not pushing one default option.

POS Systems and Hardware

Your POS system is more than just a card reader. It impacts:

Checkout speed

Employee efficiency

Reporting accuracy

Customer experience

Choosing the wrong POS can lock you into:

Long contracts

Expensive upgrades

Limited integrations

A proper POS recommendation should be based on your business type, not the processor’s commission structure. Flexible payment processing services allow your business to scale, integrate with existing tools, and avoid being locked into restrictive equipment.

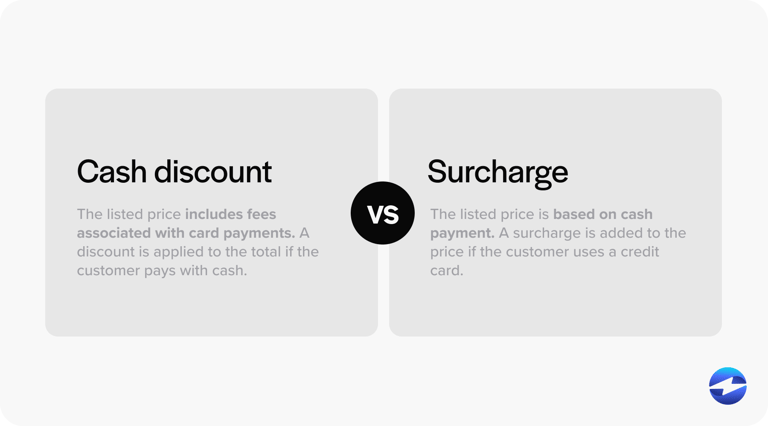

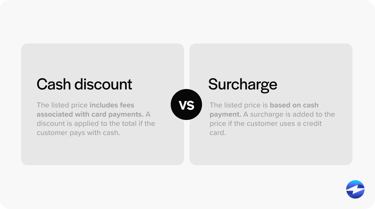

Cash Discount vs Surcharging

Many businesses look to offset processing fees, but not all programs are equal.

Cash Discount

Customers receive a discount for paying with cash. This is compliant in all states when structured correctly.

Surcharging

A fee is added to credit card transactions. This is regulated and must follow strict card brand rules.

When implemented incorrectly, these programs can create compliance risk and customer confusion. When done correctly, they can significantly reduce processing costs without harming customer trust.

PCI Compliance and Security

Security is a non-negotiable part of payment processing. Businesses must follow PCI DSS compliance standards to protect cardholder data and reduce fraud risk.

Non-compliance can lead to fines, higher fees, or loss of processing privileges.

Why Monthly Statement Reviews Matter

Most merchants never review their statements in detail. This is one of the biggest reasons businesses overpay.

A proper statement review can reveal:

Hidden markups

Redundant fees

Outdated pricing structures

Incorrect program setup

This is why Harbor Payment Solutions emphasizes education and transparency first, rather than quick sales.

Choosing the Right Payment Processor

The right processor should:

Explain your fees clearly

Match pricing to your volume and industry

Offer flexible hardware and software options

Provide real human support

Grow with your business

If a provider cannot explain your statement in plain language, that is a red flag.

Final Thoughts

Payment processing should support your business, not quietly drain it.

Understanding how transactions work, how fees are structured, and what options are available puts control back in your hands. With the right setup, many businesses can lower costs, improve efficiency, and gain confidence in their financial operations.

If you want help reviewing your current setup or understanding your statement, Harbor Payment Solutions exists to make payment processing simple, transparent, and fair.

Ready to Improve Your Payment Processing?

Start with a free consultation and see how Harbor Payment Solutions can help your business save money and scale with confidence

© 2025. All rights reserved.

Professional, transparent payment processing services for businesses across the United States. Processing services provided through trusted processing partners. Harbor Payment Solutions operates as a consulting and advisory firm.

Powered by FX Web Ventures