Payment Processing Fees Explained

Learn how payment processing fees work, what’s negotiable, and how to spot overcharges. Understand interchange, processor markups, pricing models and more.

12/18/20253 min read

Why Understanding Payment Processing Fees Matters

Payment processing fees directly affect your margins. Even a difference of 0.2%–0.5% can add up to thousands of dollars per year for growing businesses.

Understanding your fees helps you:

Spot unnecessary or inflated charges

Compare processors accurately

Negotiate better terms

Choose the right pricing model for your business

For businesses new to card acceptance, learning about payment processing solutions can help clarify how fees are structured and what services are included.

The 3 Main Components of Payment Processing Fees

Nearly every credit card transaction includes three layers of cost.

1. Interchange Fees (Non-Negotiable)

Interchange fees are set by the card networks (Visa, Mastercard, etc.) and paid to the issuing bank.

They vary based on:

Card type (debit, credit, rewards)

Transaction method (swiped, chipped, keyed-in)

Industry and risk level

Key takeaway:

Interchange fees are fixed, no processor can eliminate them.

2. Processor Markup (Negotiable)

This is where processors make their money.

Markup can appear as:

A percentage (e.g., +0.30%)

A flat per-transaction fee (e.g., +$0.10)

Monthly account fees

This portion can be negotiated, and it’s where overcharging most often occurs.

3. Additional & Hidden Fees (Often Overlooked)

These are commonly buried in statements and contracts:

PCI compliance fees

Monthly minimums

Statement or platform fees

Batch fees

Early termination fees

Many businesses don’t realize they’re paying these until they’re pointed out.

If you’ve ever looked at your monthly payment processing statement and thought, “I don’t know what half of this means”, you’re not alone.

Many businesses unknowingly overpay in processing fees simply because the pricing structure is confusing by design. In this guide, we’ll break down exactly how payment processing fees work, what’s negotiable, and how to tell if you’re being overcharged.

Common Pricing Models Explained

Interchange-Plus Pricing (Most Transparent)

Best for: Most small to mid-sized businesses

You pay:

Interchange (pass-through)

A clearly defined processor markup

This model is predictable, auditable, and transparent.

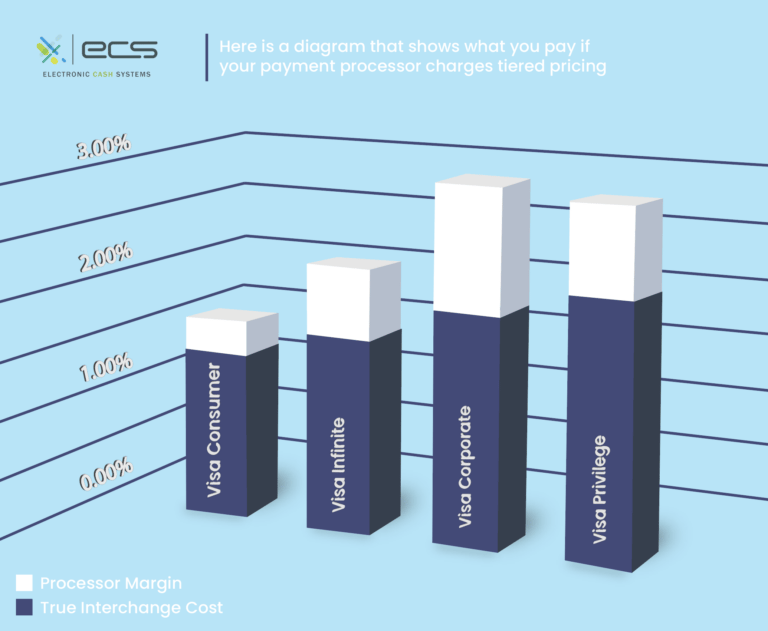

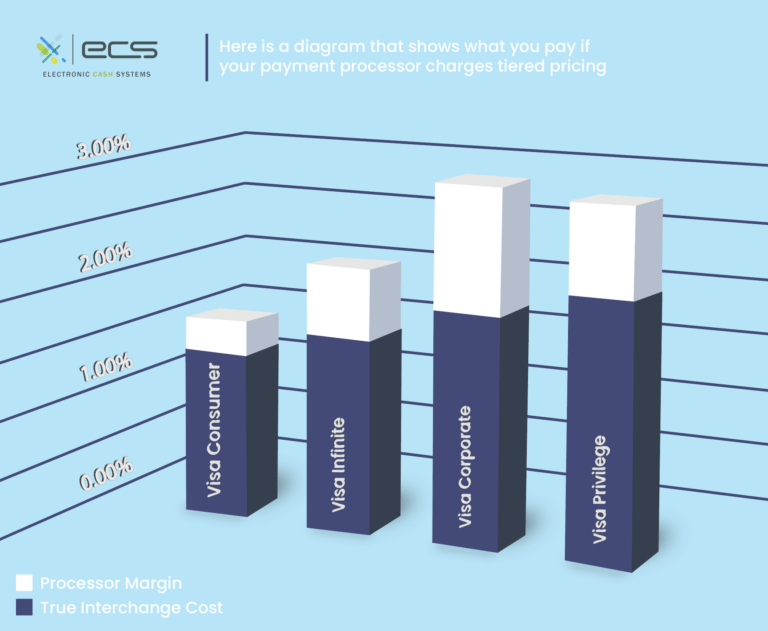

Tiered Pricing (Often Confusing)

Transactions are grouped into “qualified,” “mid-qualified,” and “non-qualified” tiers.

Downside: Processors decide what falls into each tier, often resulting in higher costs.

Flat-Rate Pricing (Simple, But Not Always Cheapest)

Popular with new or low-volume businesses.

Example:

2.9% + $0.30 per transaction

Trade-off: Simplicity vs. potentially higher long-term costs.

Hidden Fees to Watch For

Beyond standard processing fees, many merchants encounter additional charges such as:

PCI compliance fees

monthly minimums

statement fees

batch fees

Understanding PCI DSS compliance standards can help businesses determine whether these fees are legitimate or unnecessary.

Why Reviewing Your Processing Statement Matters

Most merchants never take a close look at their monthly processing statements. Over time, small pricing changes or hidden fees can quietly cost thousands of dollars.

A free payment processing review allows business owners to identify overcharges, negotiate better pricing, or switch to a more transparent structure without disrupting operations.

How Much Should You Be Paying?

There’s no universal “perfect rate,” but most businesses fall within a reasonable range depending on:

Monthly volume

Average ticket size

Card mix (debit vs. rewards cards)

Industry risk profile

The key is knowing what’s normal for your business type, not just accepting the first quote you receive

How to Lower Your Payment Processing Costs

Reducing processing costs does not always require switching providers. Often, small changes such as adjusting pricing models or eliminating redundant fees can have a meaningful impact.

Businesses exploring cost-saving strategies may also consider cash discount and surcharging programs, which can offset processing expenses when implemented correctly.

Understanding state-level surcharging regulations is essential before adopting these programs.

Final Thoughts

Payment processing fees should be understandable, transparent, and aligned with your business model. When fees are unclear, businesses lose control over one of their largest recurring expenses.

If you want help evaluating your current setup, exploring better pricing options, or learning more about payment processing services, you can contact our team for guidance.

Ready to Improve Your Payment Processing?

Start with a free consultation and see how Harbor Payment Solutions can help your business save money and scale with confidence

© 2025. All rights reserved.

Professional, transparent payment processing services for businesses across the United States. Processing services provided through trusted processing partners. Harbor Payment Solutions operates as a consulting and advisory firm.

Powered by FX Web Ventures